Happy Independence Day! 🇮🇳

As India turns 75 there are many things on the economic front that we can be proud and optimistic about. One of them is that today India is comfortably placed on its foreign currency reserves. It can pay for its imports and honor its external debt obligations with ease. This was not the case in 1991 when we had to go to the IMF for an emergency loan. It is also not the case today, with our neighbours in the subcontinent. What changed for India between 1991 and now? What is the difference between us and our neighbours on the subcontinent today?

By the way, it is not just the subcontinent that is facing these headwinds. Developing economies around the world are under stress. Inflation is high and many countries haven’t fully recovered from the pandemic. On top of it, since most developing countries are net importers of oil, their imports have shot up, depleting foreign exchange reserves and weakening currencies.

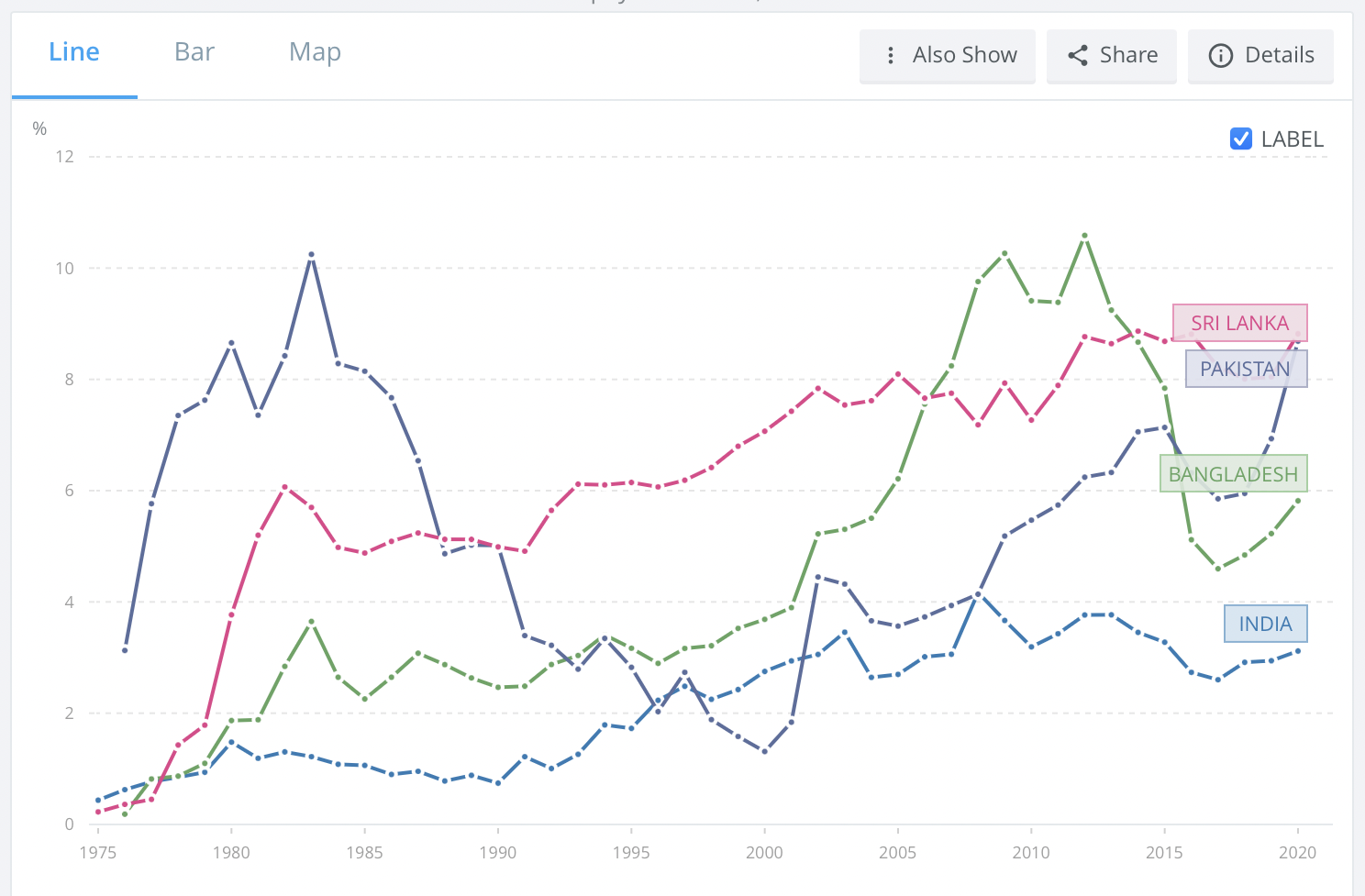

Matters are quite grim in our neighbourhood. Sri Lanka is essentially in default. Pakistan will need an IMF rescue package. Even Bangladesh, which has done so well economically, has asked for help from the IMF.

But India appears to be on solid ground. Raghuram Rajan, former RBI Governor, recently said that India was in no danger of following Sri Lanka or Pakistan. That is good news indeed. But the question is why? India’s economy has not done particularly well during and after the pandemic. And oil and petroleum products are still imported in massive amounts. So what’s the difference between India and its neighbors?

The answer to this question lies in India’s world-class IT & ITES (IT Enabled Services) industry.

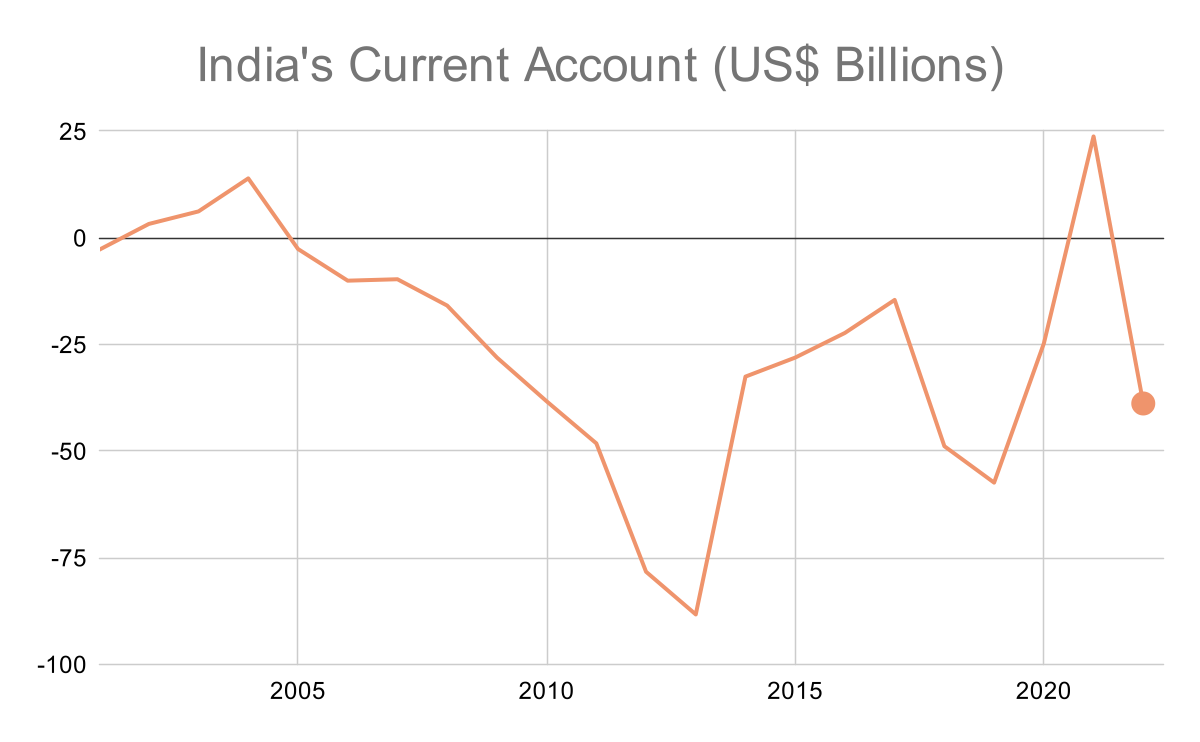

A country’s ability to pay off external debt, or import say, oil, depends upon its Balance of Payments – the net inflow or outflow of foreign currency from the country. The most important component of the Balance of Payments is the Current Account. This is how India’s Current Account has trended since 2001.

Source: RBI

Not bad. The Current Account deficit has stayed well under $100B for most of this period, even registering a smart surplus in FYE 2001. However, in FYE 2002 the Current Account deficit widened sharply to $39B. What happened?

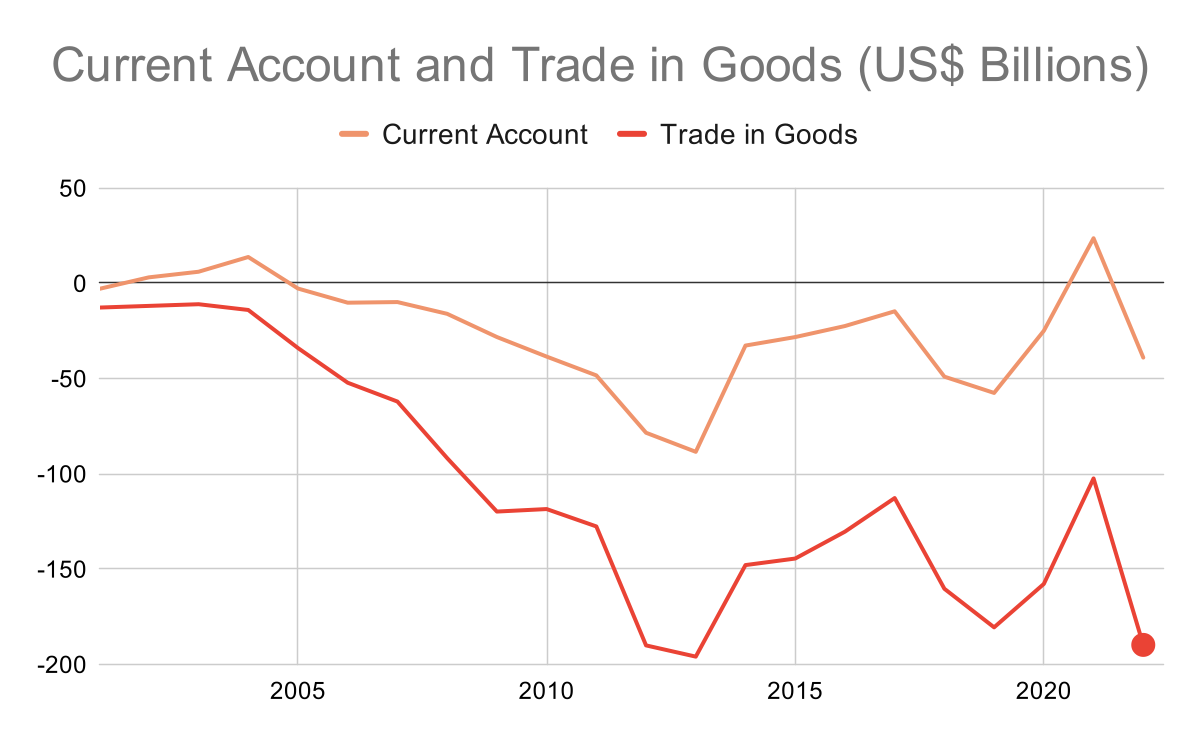

Source: RBI

The Current Account has many components. Trade in Goods, or Balance of Trade, is the most important one, for most countries. For India, this is also the most volatile component, with large deficits.

As much as 50% of Trade in Goods is attributable to net outflows of Oil and Petroleum Products. As we know, oil prices shot up after the recovery from the pandemic and then the war in Ukraine broke out. This took India’s Trade in Goods into deep negative territory.

But the Current Account still doesn’t look too bad. Even in FYE 2022 it was only 1.27% of GDP. On the other hand, the Current Account deficit in CY 2021 for Sri Lanka was 3.9% and for Pakistan was 3.5%.

Source: RBI

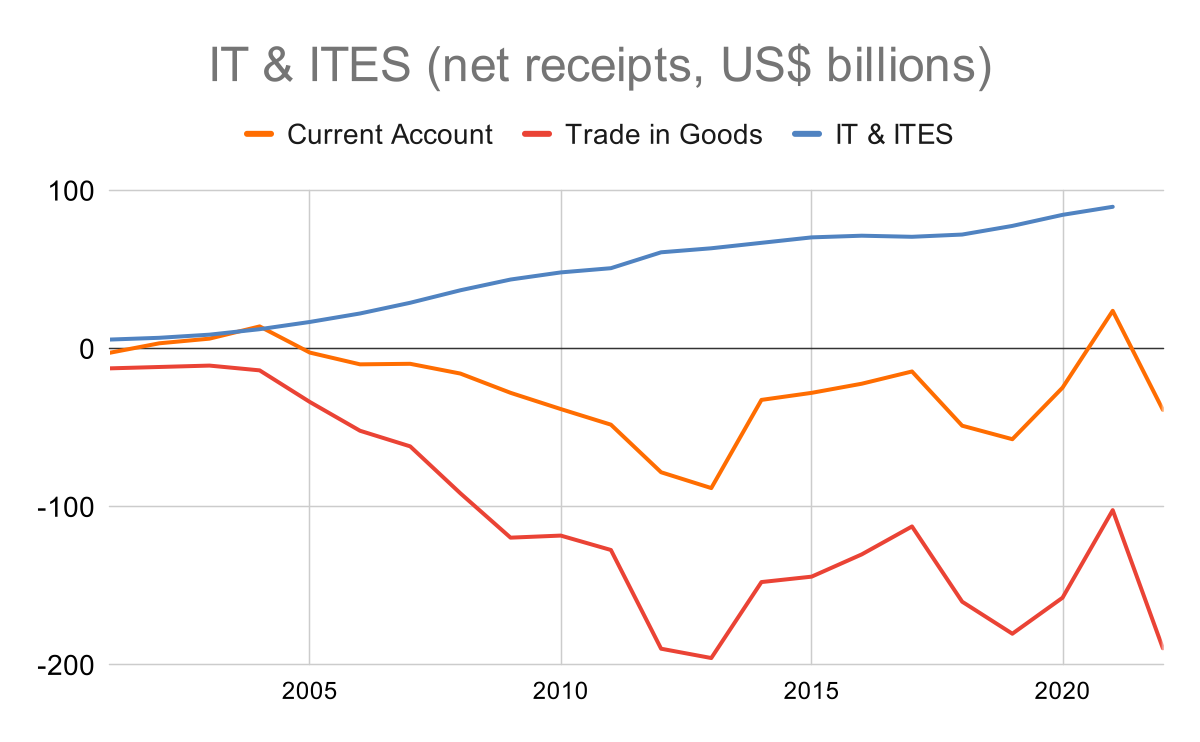

What has insulated India’s Current Account from the oil price shock?

Much of it can be explained by the forex-spinning IT & ITES industry. The blue line in the chart above represents the net receipts of the IT & ITES industry. With a smoothly rising trend line that now brings in nearly $100B in foreign exchange a year, it cancels out much of the deficit from Trade in Goods. Growth in the IT & ITES industry may slow down for a year or too, but it has none of the volatility of Trade in Goods.

Source: RBI

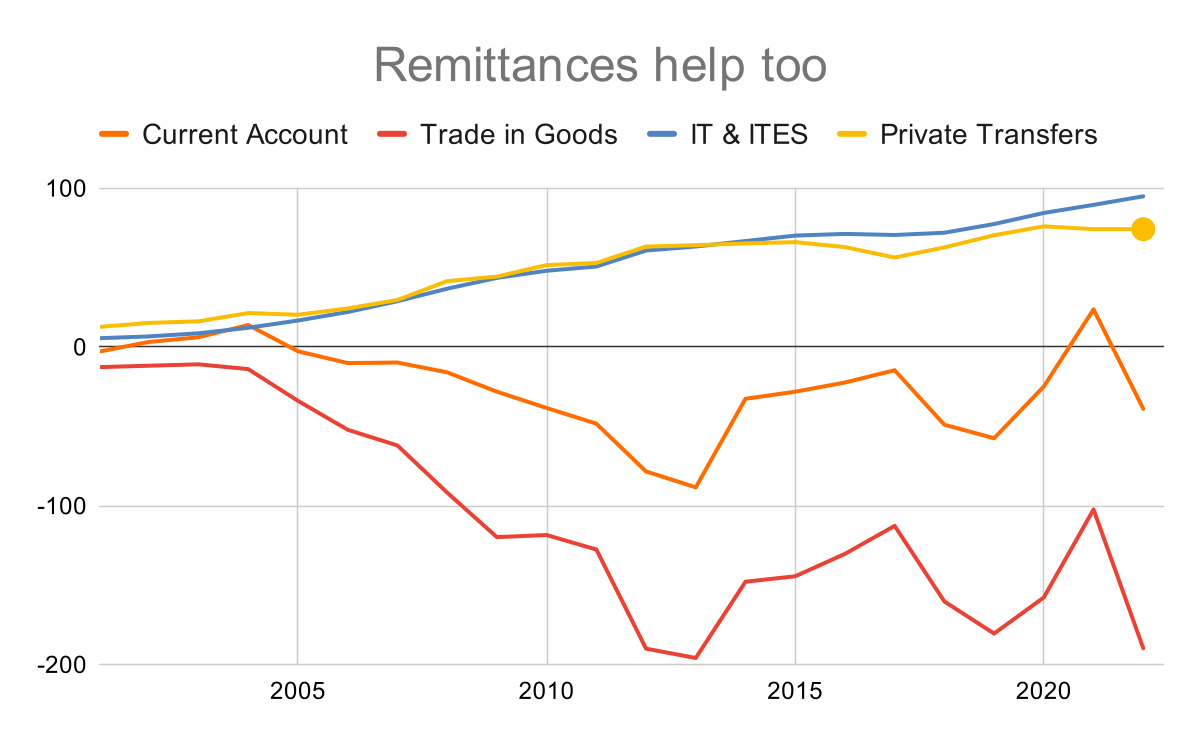

Private Transfers, which are mostly remittances from NRIs and OCIs, have also been a reliable source of forex for the country. However, remittances are not the difference between India and its neighbours. According to World Bank data, Pakistan, Bangladesh and Sri Lanka all have higher personal remittances as a % of GDP.

Source: World Bank

Remittances come in from NRIs and OCIs in many countries. It would be fair to say that a large if not a majority of the remittances from countries like the US, the UK and Australia are from workers employed by the IT industry. It is hard to estimate how much with any precision, but it is possible that something like 15-20% of all remittances could be attributable to employees in the IT industry.

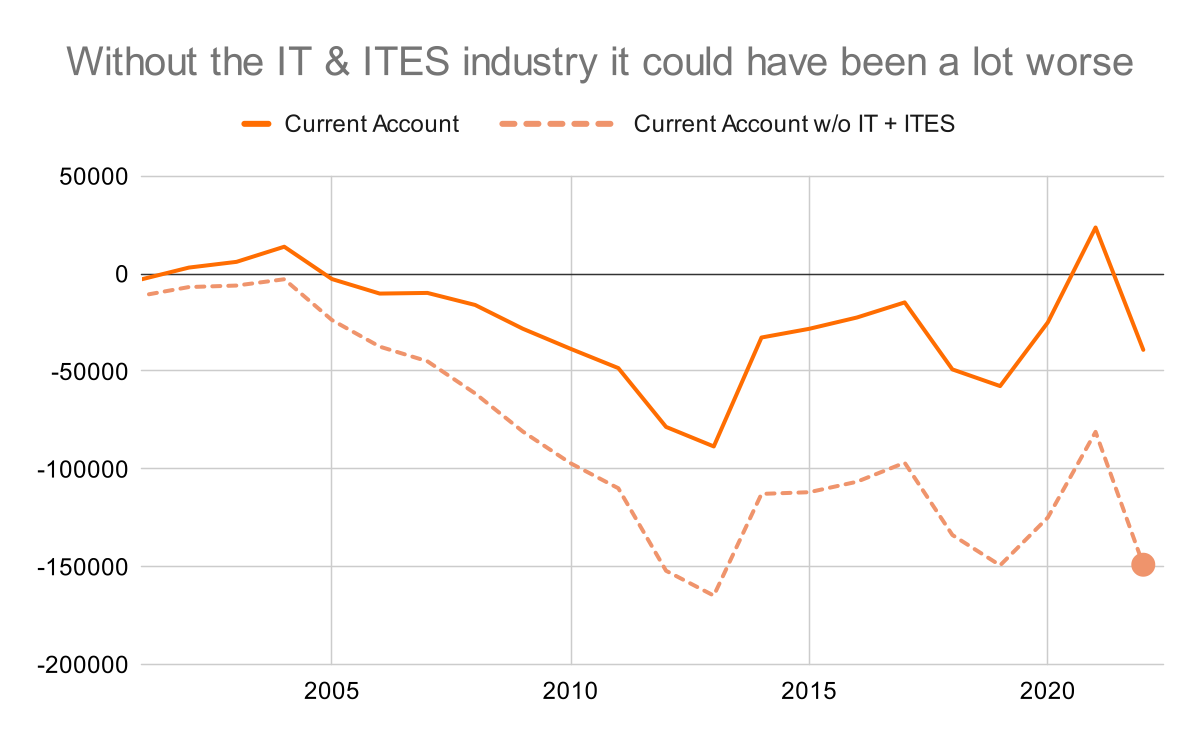

Let’s step back and look at the big picture. Imagine if India did not have an IT industry. Imagine that by some quirk of fate our industry had not taken off the way it did. What would our Current Account deficit have looked like without it? Now, I understand that an economic system is too complex to just take out an entire industry and expect that nothing else will change, ceteris paribus. For example, without the IT & ITES industry there would have been far fewer cars on the roads of Indian cities which would have reduced our oil import bill. I understand that.

But still, as a first order of approximation, if you were to just back out the IT Industry’s net contribution to the Current Account balance, what would it have looked like? We can ignore any remittances attributable to the industry.

Source: RBI

In short, very bad. The Current Account deficit would have widened to almost $150B, or 4.9% of GDP in FYE 2022. If you compare it with the same figures for Sri Lanka (3.9%) and Pakistan (3.5%) you realize what a deep hole we would have been in.

I’m glad we have a successful, thriving IT & ITES industry. In 1991, when India had to accept an IMF bailout, the industry was barely a blip on the radar. Since then it has gone from strength to strength and today stands tall as a significant contributor to India’s GDP as well as the backstop to India’s Balance of Payments. Thanks to it, India will not have to seek a bailout, now, or hopefully ever in the future.